In the late 1990's while working with a top retail broker, at what was then Smith Barney, a successful client named Dr. Goldstein would call in each day and weigh in with his market prognostications. Dr. Goldstein did quite well by buying each dip. That is, until the Dot.Com bubble burst. He was wedded to his views and did not bend to the market when conditions changed. The good doctor had margin calls and lost 60% in his account that year.

Fast-forward to the present day...

I have a friend who has done quite well being long the indexes the last 18 months. He profited handsomely by buying each dip aggressively. While very smart, he has become complacent, and I daresay, a bit arrogant about his Buy and Hold strategy. I could not help but think of Dr. Goldstein during our recent text exchange. The facts have changed, but he has refused to acknowledge the change in backdrop, instead, holding steadfast to his bullishness.

We have always attempted to operate from a flexible viewpoint, utilizing Stevie Cohen’s framework:

“What would cause you to change your opinion on your thesis, and thus, your positioning?”

Well, here is what we are seeing and why we feel this tape has become very dangerous near-term and is on the verge of becoming challenging from an intermediate-term perspective.

First off, let’s examine breadth. Breadth topped in late November. Best-observed on the NYSE Common Stock Only AD Line, note how it is acting similarly to when breadth topped in late 2021, two months before the market began a marked descent throughout 2022:

Quick side note: The Common Stock Only AD Line is one of our favorite indicators as it is one of the purest indications of what is happening underneath the hood of the market. We therefore track it weekly, looking for important positive and negative divergences where an intermediate term/long-term change in trend is poised to manifest. We feel as though the market could be on the cusp of one of those moments.

Here is what breadth is looking like this morning, as of 11:18am: Note the surge in New 52wk Lows on the Nasdaq, the widest dispersion relative to New 52-week highs we have seen in months. New 52wk Highs topped with breadth in late November. Now, New 52wk Lows are inflecting:

The Nasdaq New Highs/New Lows Index is another favorite indicator that helps us to stay honest to our process – step on the gas when in favorable territory and be defensive when we are firmly entrenched below 0, like now. These are levels pointing to a dangerous short-term backdrop.

Until we see New Highs begin to work again, our process is simple: Do as little harm as possible to the P&L until we observe this indicator turn back to highlighted green levels – areas where we generated an excellent 500% return last year:

As for our current positioning, one of our biggest holdings is a short in the Russell 2000 Index ($RUT). The Ishares Russell 2000 ETF (IWM) has already tested its 200day SMA intraday. A potential break of this level looks very possible in the days ahead.

While this position is primarily a hedge for our existing longs, it could also deliver alpha in the near-term, should the market begin another leg down in the coming weeks.

$214.88 is a very crucial price point.

A decisive close below this level would cause us to increase our short position further as, it would most likely, augur a more intermediate-term correction for small-caps. As Stan Weinstein has been wont to say, the Russell 2000 is the "weak sister." We always want to short the weakest index first. This is why we have hedged our existing longs with a short position in the IWM:

On the Macro front, we actually believe the Fed ought to be raising rates NOT lowering them. We think many market participants like my bullish friend are too cavalier about the Fed. There is a good chance Powell's time at the Fed will soon be coming to end, that Trump will surely pick a Fed chief more inclined to let inflation run hot. Powell will not want his legacy tarnished by missing another upturn in inflation.

While wage gains did not inflect upwards in today's super-strong jobs report, this part of the inflation picture is poised to do so as Trump's executive orders take shape in late-January. Make no mistake. Losing a few million migrant workers will squeeze an already tight labor force even further. It will drive wage gains higher. What’s more, tariffs are highly inflationary too.

The Daily Spark had a great piece on Inflation Reaccelating the other day. Hat tip to Torsten Slok & Co!

From a cycle perspective, long-term rates are still way too low for an economy this strong. Consider that the economy under Trump is poised to accelerate even further, as his anticipated corporate tax cuts should spur a big domestic CAPEX cycle AND another wave of big hiring (seeing this in real time today).

The most important chart right now is the 10-Year Treasury Yield ($TNX). For us, it’s not whether the $TNX is heading above 5%, the more salient question is WHEN?!!:

After spending 2024 digesting the big move up in rates from 2021-2023, the $TNX looks poised to stage an important break out above 5%. If we had to guess, we think it will occur this Spring, as the impact of Trump’s inflationary economic policies become evident. Just a guess.

In the very near-term, the muted reaction to the 10-Year’s move to 4.76% informs us the breakout above 5% may take some time before it manifests. Time will tell.

Of course, we are open to the possibility our analysis is incorrect and the 10-year does NOT take out 5% decisively. That is not our job. We are just spit-balling here.

Our job is to present Top Tier Inflection Points. In this vein, we are more bullish than ever on our process. Remember, this is an exclusive club to help make you money during the good times. But we also do our best to keep you out of trouble in the bad and treacherous periods.

As such, periods of market chop and market corrections are where we do so much of our best work, as we go into deep research mode. Keep in mind, the best Top Tier Inflections will turn up BEFORE the market does. This is why our results always reflect the best alpha AFTER market corrections and bear markets.

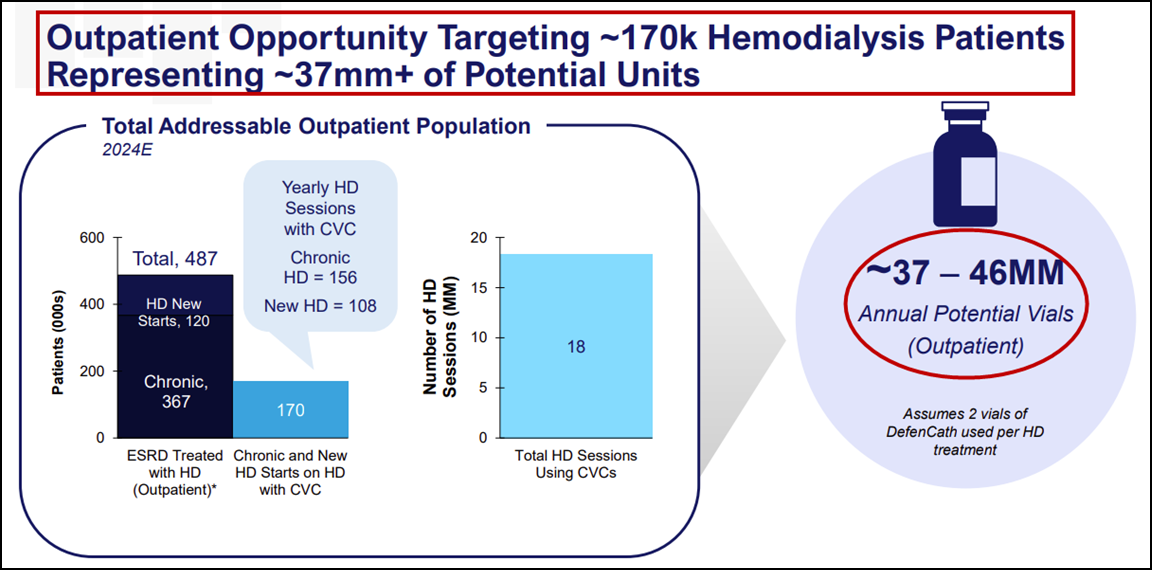

A new position we are very bullish on is a med-tech company called CorMedix Inc. (CRMD). CorMedix's DefenCath stands to become the next STANDARD OF CARE to stem infections that occur during kidney dialysis treatments:

CorMedix already has 60% of the Outpatient Market locked up, with 4 of the Top 5 players all onboard as customers:

On January 7, CorMedix pre-announced a huge beat for Q4 and also referenced continued strong uptake in demand in Q1:

CorMedix reports preliminary Q4 net revenue $31M (~$11M above consensus. EBITDA of $12M was 250% above consensus too) and approximately $43M for FY 2024.

The Company is shipping DefenCath to all three of its midsized dialysis operator customers and has seen continuous ordering of increasing size throughout the quarter. CorMedix has more than $25M of existing open purchase orders scheduled for delivery during the first quarter of 2025.

The CorMedix team is actively working with its Large Dialysis Operator customer to begin DefenCath implementation in the first half of 2025, and hopes to achieve the LDO's targeted patient utilization of 4,000 patients in H2 2025. The Company announces an expanded deployment effort in the inpatient hospital segment beginning in Q1 2025.

Looking ahead, we think forward numbers are too low. As such, we have established a 7% position in the accounts we oversee.

Based on the current momentum in CRMD’s business, we think the Street has yet to incorporate the big uptake set to manifest at its biggest customer (who is either Davita or Fresenius). As such, we attach 70% odds that the current consensus we see for 2027-2028 will actually materialize in 2026 and 2027.

Outsized revenue and earnings growth is set to manifest in the coming quarters. Assuming it breaks through recent highs/resistance at $14, we expect a move to the mid-to-teens quickly thereafter. This is a long-term position for us, NOT a short-term trade.

We are still long a small 1.5% long-term position in Nebius Group NV (NBIS). It acts super well and is demonstrating the type of relative strength we look for during market corrections.

For those that did not see it, CrossRoads Capital had a very thoughtful piece recently on NBIS. We love the strong accumulation 4 of the past 5 days:

We have a 4% weighting in our long-term position in Byrna Technologies (BYRN). The company's most important new product cycle will kick in this Spring with the releases of its Compact Launcher. This is a non-lethal gun that will be 40% smaller than its current offerings, opening up a swatch of new consumers to the company's products.

Women will be able to fit them into their purses and men can slip them into their suit jackets. Consumers love their products and we think 25% of their 600k customer-base will return to buy this new version, creating a HUGE UPGRADE CYCLE for Byrna.

Looking ahead, we think BYRN will do revenues of $135M in FY25 vs $110.68 estimates, and $200M+ vs $134.85 estimates in FY26, BLOWING AWAY CONSENSUS:

NANOPHASE TECHNOLOGIES CORP (NANX)

Within the nano-tech space, we are very bullish on Nanophase Technologies Corp. (NANX) and its long-term prospects. Nanophase is an unknown disruptor where major tailwinds have finally lined up, positioning them for a couple of impressive years ahead.

We think it has multi-bagger potential and are therefore slowly building a nicely-sized position in NANX.

Nanophase has patented a process whereby its zinc-oxide ingredients have become a key white label ingredient solution for an assortment of “clean” beauty products that are free of harmful chemical additives. The company’s solutions are safe and also enhance the appearance of the skin. NANX has won 3 Best In Beauty awards the last two years, spurring an inflection in demand for their products.

The proof is in the pudding.

Rare to find this type of strong, organic top-line growth married to incredible operating leverage in its model. Please take a look:

While NANX is extremely illiquid, given the company could eventually scale their long-term revenues to $500M – per its last conference call – we see strong potential for NANX to be a 5-10 Bagger over the next 2-4 years.

With orders up 80% YoY entering 2025, we think NANX can do $85M in revenues this year and earn $0.20-$0.25. The strong growth will continue in 2026, with the potential to do $125M and earn $0.40 next year. Should such a ramp materialize, we think NANX could 3x the next 18 months.

Turning to the cyber security space, we are highly intrigued by the incredible relative strength being exhibited by Allot Limited (ALLT). Allot may have landed a HUGE cyber-security deal with Verizon. If so, the stock could double or triple from current levels. We are working on diligently behind the scenes.

In the meantime, here is a solid summary piece from Seeking Alpha to help you get up to speed.

While we think the article’s numbers are way too high, there is no denying the incredible relative strength in the stock of late. It just does not go down. That always gets our attention.

What also really has our attention is the tangible upside-potential of Profound Medical Corp. (PROF) to become a multi-bagger from current levels over the next 18-36 months.

Profound Medical has a disruptive MRI technology that is poised to see rapid adoption this year after securing BEST-IN-CLASS reimbursement for its therapeutic platform for BPH and Prostate Cancer. The company has a Top Tier CEO/Chairman in Arun Menawat, who has a wonderful long-term track record. Menawat was very bullish about Profound’s growth prospects in a press release a few days ago:

“In light of the fact that 2024 marked the final year in which we were operating in a primarily patient-pay environment for TULSA, we were excited to see adoption of TULSA-PRO® continue to increase…

Now, with the strengthening of our balance sheet via the completion of our underwritten public offering of common shares in December, and, as of last week, the TULSA procedure being uniquely reimbursed both at Urology APC Level 7 and at an unrivalled number of treatment settings, we believe that we are on the cusp of entering into a stage of escalating growth.”

We have been tracking PROF behind the scenes for four years. We are long a small 1% position in the name and are actively doing our due-diligence on the company now.

Profound has secured reimbursement that is 25% higher than that received by the Da Vinci procedure, which is the current standard of care for Prostate Cancer remediation. What’s more, PROF also received reimbursement in ALL settings, including within individual urologist settings.

Finally, the patient side effects associated with Profound’s TULSA device are so much less invasive than those experienced with the Da Vinci – a huge factor that should spur accelerated adoption in the coming quarters.

Lake Street's Ben Haynor has also done some excellent work on PROF.

The key takeaways are that the economics are much better for hospitals to now adopt Profound's TULSA solution, even with its upfront price tag of nearly $350K. Please take a look:

What really intrigues us are the out-year numbers. PROF is already doing ~70% of its revenue mix via consumables. This Razor/Razor-blade model should prove very profitable for Profound once they cross the chasm to profitability.

Take a look at the forthcoming ramp. We attach 70% odds these numbers can take shape, making PROF an execution story from here:

We are the first to admit that things can change quickly. What is now a chop-fest market could easily deteriorate into a worse tape, or conversely, quickly improve. We will let our process guide us. In particular, when we see a spate of fresh breakouts materialize in Top Tier Inflections we plan to be on top of them as they manifest.

Until then, we will be continuing our research behind the scenes. Our best guess is the market will be stuck in this land of chop through the end of January, at a minimum. In a worse case scenario, we could see a more extended correction of 2-4 months, OR LONGER, particularly if we see the 10-Year J-Curve strongly through the 5% levels delineated earlier. And, of course, the uptrend could resume if Trump’s economic policies prove to be more moderate and less inflationary.

While we still have our noted long-term smaller positions, we are not taking size in anything new in the current backdrop, preferring high levels of Cash in our accounts and the accounts we oversee.